By, Jon Duncan, Head of Responsible Investment, Old Mutual Investment Group

Read Part One: Jon Duncan, Old Mutual’s Head of Responsible Investment Writes About COP21 and the Effects of Carbon on an Investment Portfolio

The issues that are important for investors to consider in respect of climate change include: the current state of intergovernmental negotiations; its long-term physical impacts; the likelihood of assets becoming stranded; the emergence of new technologies and opportunities; current market responses; and, importantly, the timeframes over which these might occur.

This is a brief exploration of how these issues may inform the macrothematic economic outlook, along with more sector- and stock-specific calls.

SOUTH AFRICAN CLIMATE ACTION AND INSIGHTS

South Africa (SA) has committed to reduce emissions by 34% from its business-as-usual trajectory by 2020, and by 42% by 2025, conditional on the aforementioned international technological and financial assistance. It has pledged that emissions will peak, plateau and then decline (PPD) out to 2050, with a peak emissions range of 614 megatonnes (Mt)/year. The PPD model provides investors with a rough guide to what SA’s carbon budget will potentially look like. Based on the current emissions profile and the energy build programme proposed in the Integrated Resource Plan (IRP), it is possible to do basic modelling on the extent to which investments being made today are likely to fit within SA’s long-term carbon budget.

This not only informs the debate around long-term asset stranding, but also supports an analysis of whether our current energy build programme is aligned with SA’s stated long-term carbon reduction goals.

Along with national policy commitments, the SA Government has published a draft Carbon Tax Bill and, although its implementation date is uncertain (due to recommendations made by the Davis Tax Commission), when promulgated, it will force companies to internalise the costs of GHG emissions, and thus create an incentive for mitigation action. Understanding the framework of the proposed Carbon Tax Bill and the likely price impacts will be important for investors in SA.

Already some 80% of the world’s carbon emissions carry a price through national and regional carbon trade or tax schemes. Thinking that SA can continue to have no price for carbon in our economy is unrealistic, and the sooner investment managers understand this, the better for their clients.

CARBON BUDGET AND STRANDED ASSETS

Another important aspect of the negotiation is the consensus established in 2010 at COP16 in Cancun. Here, 193 countries (including the US, China and SA) agreed that we should aim to limit the most serious consequences of global warming by ensuring that the global average temperature rises to no more than 2°C above pre-industrial levels. Two degrees doesn’t sound like a lot, but the Earth’s biophysical system is sensitive to a rising temperature, much like a human body is.

The temperature rise thus far is around 0.85 degrees, and progress towards the 2°C threshold can be tracked through measuring the increasing concentration of carbon dioxide (CO2) in the atmosphere – measured in parts per million (ppm). This has been measured daily since 1958, and plotted on the now-famous Keeling Curve – currently we sit at just above 400ppm, with a 30 November reading of 400.75ppm.

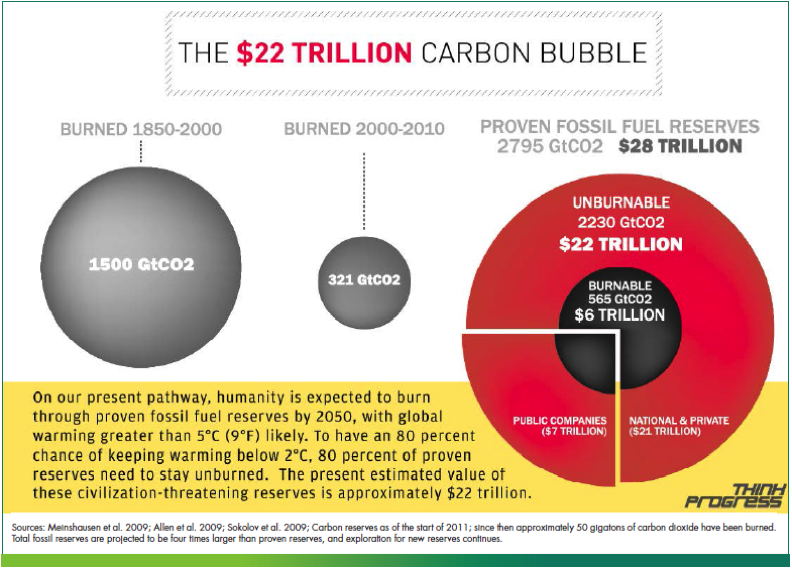

Using our knowledge of the volume of the atmosphere, ppm readings and current emission rates, it is possible to calculate the amount of CO2 that can still be emitted before we hit the 2°C threshold, popularly termed the Global Carbon Budget. Central to the Paris negotiations is, of course, who gets which piece of this pie.

The Global Carbon Budget has been the subject of analysis by the World Resources Institute and the NGO, Carbon Tracker, both of which indicate that the proven and probable fossil fuel reserves reported as assets on the balance sheets of the World’s largest resource companies, are well in excess of what science is telling us we can safely still burn. This situation creates the potential for a carbon bubble and a high occurrence of stranded assets in the world’s cumulative listed equity portfolio, which has material implications for long-term asset pricing in the market.

Investment managers use carbon footprinting to understand their portfolios’ exposure to long-term carbon risk and the potential for asset stranding. It also provides insight into which companies and sectors carry the most carbon risks, and serves as a solid platform for engagement with underlying companies regarding reduction and disclosure practices. Read more about Old Mutual’s carbon commitment and Montreal Pledge disclosure here: www.oldmutual.com/climatechange.

HOW DOES THIS TRANSLATE?

The movement towards portfolio decarbonisation in developed markets is quite well advanced, with US and European asset owners supporting the divestment campaign. But, as we have seen, it is not so straightforward for developing markets. In SA, awareness among institutional investors is growing, as pension fund regulation, media attention and COP21 point to the urgent need to mitigate risks in their equity

portfolios. According to the African Development Bank, the opportunity that emerges for investors in SA and Africa generally lies in the real asset space, where the annual infrastructure investment required is around US$95 billion to 2050.

As the largest private sector investor in African infrastructure, Old Mutual has the expertise, scale and in-country presence to unlock this opportunity in a way that generates market-related returns and delivers socioeconomic benefits, while being cognisant of the impact we have on the quality of the environment, and of the legacy we leave for future generations. To date, on behalf of our clients, we have invested over R12.5 billion in renewable energy, R1.2 billion in education, R9.1 billion in housing, and R1.5 billion in sustainable agriculture.

Old Mutual Investment Group (Pty) Limited (Reg No 1993/003023/07) is a licensed financial services provider, FSP 604, approved by the Registrar of Financial Services Providers (www.fsb.co.za) to provide intermediary services and advice in terms of the Financial Advisory and Intermediary Services Act 37 of 2002.

Contact details

Jon Duncan:

Email: [email protected]

Web: www.oldmutualinvest.com