Major Drivers and Trends in SRI Investing Growth

Sustainable Responsible Impact Investing Grows 33% in 2 Years

Jan 24, 2017 9:55 AM ET

Major SRI Drivers and Trends from the SRI Trends Report

In recent years, numerous trends have shaped the evolution and growth of SRI within US financial markets:

- Money managers increasingly are incorporating ESG factors into their investment analysis and portfolio construction, driven by the demand for ESG investing products from institutional and individual investors and by the mission and values of their management firms. Of the managers that responded to an information request about reasons for incorporating ESG, the highest percentage, 85 percent, cited client demand as a motivation.

- However, 114 money managers reported little to no detail for ESG assets worth $5.38 trillion, much of it identified through their PRI Transparency Reports. These managers did not provide information on the specific products that were subject to ESG criteria and generally divulged few if any details on the specific ESG criteria incorporated.

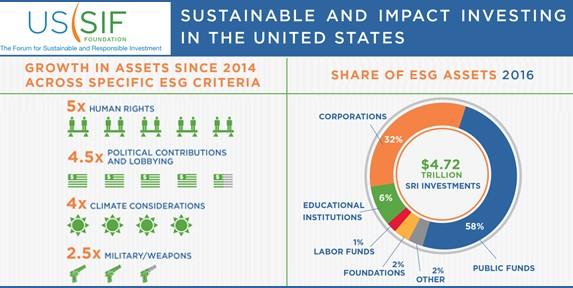

- Of the money managers that responded to a question in the US SIF Foundation survey about their ESG incorporation strategies, 62 percent reported that they use some combination of negative screening, positive screening and ESG integration within their funds. More than half reported using strategies of impact investing and nearly half used sustainability themed investing as a strategy. The incorporation strategy that affected the highest number of assets, $1.51 trillion, was ESG integration. (See the glossary of ESG incorporation terms below.)

- Climate change remains the most significant overall environmental factor in terms of assets, affecting $1.42 trillion in money manager assets and $2.15 trillion in institutional investor assets — more than three times the amounts affected in 2014. Fossil fuel restrictions or divestment policies applied to $152 billion in money manager assets and $144 billion in institutional investor assets at the beginning of 2016.

- Moreover, shareholders concerned about climate risk filed 93 resolutions specifically on the subject in 2016 and negotiated a number of commitments from the target companies to report on strategic planning around climate change or to reduce their greenhouse gas emissions.

- When it comes to specific ESG criteria, conflict risk analysis, including the exclusion of companies doing business in countries with repressive regimes or state sponsors of terrorism, holds the most weight for money managers, with $1.54 trillion in assets affected, and it remains the top ESG factor institutions incorporate into their investments, affecting $2.75 trillion.

- An issue tracked for the first time this year was transparency and anti-corruption: money managers reported $725 billion in assets taking this criterion into account, while institutional investors reported $528 billion.

- The emerging trend of gender lens investing, tracked separately for the first time this year, was identified as affecting the management of nearly $132 billion in money manager assets, and $397 billion in institutional investor assets.

- Community investing institution assets jumped 89 percent, from $64 billion to nearly $122 billion. This growth was led by a particularly large increase in the assets of community development credit unions, which more than doubled since 2014.

- As shown by the number of proposals filed each year, disclosure and management ofcorporate political spending and lobbying is the greatest single ESG concern raised by shareholders, with 377 proposals filed on this subject from 2014 through August 2016. Many of the targets of these proposals are companies that support organizations that deny climate change science and undertake lobbying against regulations to curb greenhouse gas emissions.

- Investors filed 350 proposals at US companies from 2014 through 2016 to facilitate shareholders’ ability to nominate directors to corporate boards. As a result of the strong investor support for these “proxy access” proposals, the share of S&P 500 companies establishing proxy access measures over this period grew from 1 to 40 percent.

Read about this and more in the January 2017 issue of GreenMoney at- http://www.greenmoneyjournal.com/january-2017/major-sri-drivers-and-trends-from-the-sri-trends-report/